The industry disrupter, the future, the next everything. Blockchain has been hyped ever since it was introduced into the mainstream during the early 2010’s. From a concept born in the 90’s, as a computational practical solution for time-stamping digital documents to what we know today as a Blockchain – which is a distributed database that is shared among the nodes of a computer network. As a database, a blockchain stores information electronically in digital format which cannot be altered or doctored.

In 2019, here at Simplify Consulting we took a closer look at Blockchain in Financial Services. We explored the history, the benefits, and opportunities it could bring, along with some use cases. At the time many firms were still dipping their toes in the water, here’s some great examples:

- HSBC made their first Blockchain trade transaction

- Calastone were about to go live with the blockchain Distributed Market Infrastructure (DMI)

- Santander had become the first UK bank to introduce the technology for international payments

More industries are now adopting Blockchain technology with Banking & Financial Services accounting for 29.7% of the net total spend (Source IDC 2020). Disruptive, yes, but it’s also transformative and with the regulator’s attention on firms from a Consumer Duty perspective there still remains untapped opportunities to provide better outcomes for consumers. Distributed ledger technology (DLT) allows Wealth firms to reduce overall transaction times and costs across each part of the value chain, but there will be an expectation that some of these saves are passed to the customer.

When exploring some of the benefits it can bring, It feels it’s more a matter of when not if Wealth firms will adopt Blockchain technology – worldwide spend on blockchain solutions is forecast to reach $17.9 billion by 2024 and will grow at a compound annual growth rate (CAGR) of 46.4% according to the IDC 2020 projections. Wealth firms will struggle to serve modern clients effectively without a digitised operating model, so a move from legacy models should be a priority.

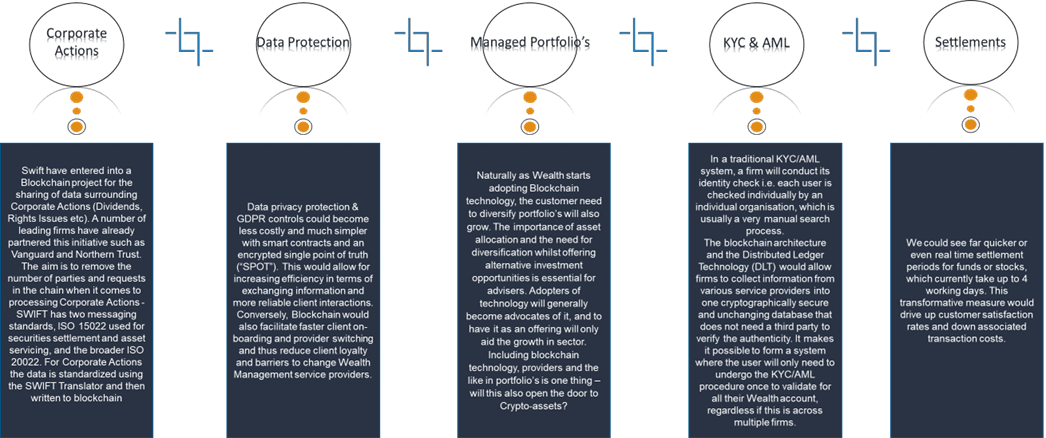

We take a closer look at just some of the potential benefits Wealth could realise:

Whilst the above carries a heavy focus towards back-office processing, there is a clear need and demand for Blockchain technology right through the customer journey. A great example of this is where McKinsey analysis found that Relationship Managers / Financial Advisors spent up to 70% of their time conducting non-advisory tasks such as administration, regulatory and compliance duties. (Source Wealth management analytics transformation | McKinsey). This identifies the need for centralised data repositories, integrated AI capabilities to capture output and process instructions with adherence to regulatory controls – thus allowing more focus time between client and advisor, which will drive the right behaviours and driving the right outcomes for customers.

FCA and regulation

With the adoption of any new technology, it’s always worth remembering that complex regulation is needed and is in place in other areas to protect firms and customers alike. There is a recognition that blockchain has the potential to deliver significant benefits, as long as the risks are managed. Overall, the FCA has supported the introduction of Blockchain, within regulated parameters – it’s believed this can also create more highly skilled jobs across the UK, boost trade, and extend the UK’s competitive edge over other leading fintech hubs. You can find more information about the review conducted by Ron Kalifa OBE here.

It’s not all been plain sailing…

It might have been expected that Blockchain was more integrated into Wealth by now and there may be some basic reasons why it’s not been adopted by the masses.

Many Blockchain projects have been referred to as “experiments” and there’s a good reason why, because many have failed and failed hard. Globally, one of the biggest failures resulted in the ASX (Australian Securities Exchange) pulling a project to upgrade clearing and settlements of shares to a Blockchain based platform – over 6 years after initiation and at a cost of over $165m, you can read more about this here.

Blockchain projects are typically reliant on existing legacy systems rather than replacing them, particularly distributed ledgers that allow a select group of firms / services such as banks or government houses to share information on an immutable record, therefore any enhancements can be timely and costly to construct, but this isn’t the only area may be preventing the growth in wealth.

- Technology Understanding The primary challenge associated with blockchain is a lack of awareness of the technology and how it works. Not understanding its capabilities has a direct impact on investment and the exploration of ideas.

- Culture Shock Heavily manual processes, dependencies on third parties and reliance on legacy systems are typical of where we stand today in Wealth, but there is a sense of control and oversight. Blockchain represents a total shift away from the traditional ways of doing things. It places trust and authority in a decentralised network rather than people, teams and firms working together. This loss of control and oversight will be a major concern for many.

- Security While cryptocurrencies offer anonymity (transactions are linked to wallets rather than to individuals), many potential applications of the blockchain require smart transactions and contracts to be indisputably linked to known identities, and thus raise important questions about privacy and the security of the data stored and it’s accessibility.

- Implementation costs the costs to implement Blockchain remains an unknown and could easily spiral (as mentioned in the ASX case). Introducing Blockchain requires industry expertise, time and the right resource to help realise the benefits of adoption. With shrinking budgets, short delivery expectations and risk of not getting it right – firms are more averse to including them in TOR’s.

In summary, there’s an endless array of benefits Blockchain could bring to Wealth. It is not yet clear if the industry is ready for these changes or if Blockchain is deemed the right solution. Blockchain will take firms into a new era for technology, a place which puts the customer at the forefront, a place which can take automation to the next level. For many this will be unchartered territory, especially those who are still heavily reliant on aged technology stacks from long periods of under investment.

Coming Soon: We explore the future of Wealth Operations and what the landscape will look like in the next decade. Do you think Blockchain will be part of this?

..

Chris Lamb

Wealth Consultant