With the consultation period for the FCA Policy Paper on ‘Advice Guidance Boundary Review proposals for closing the advice gap’ now closed, will the proposals provide a solution to the long-standing issue of the advice gap?

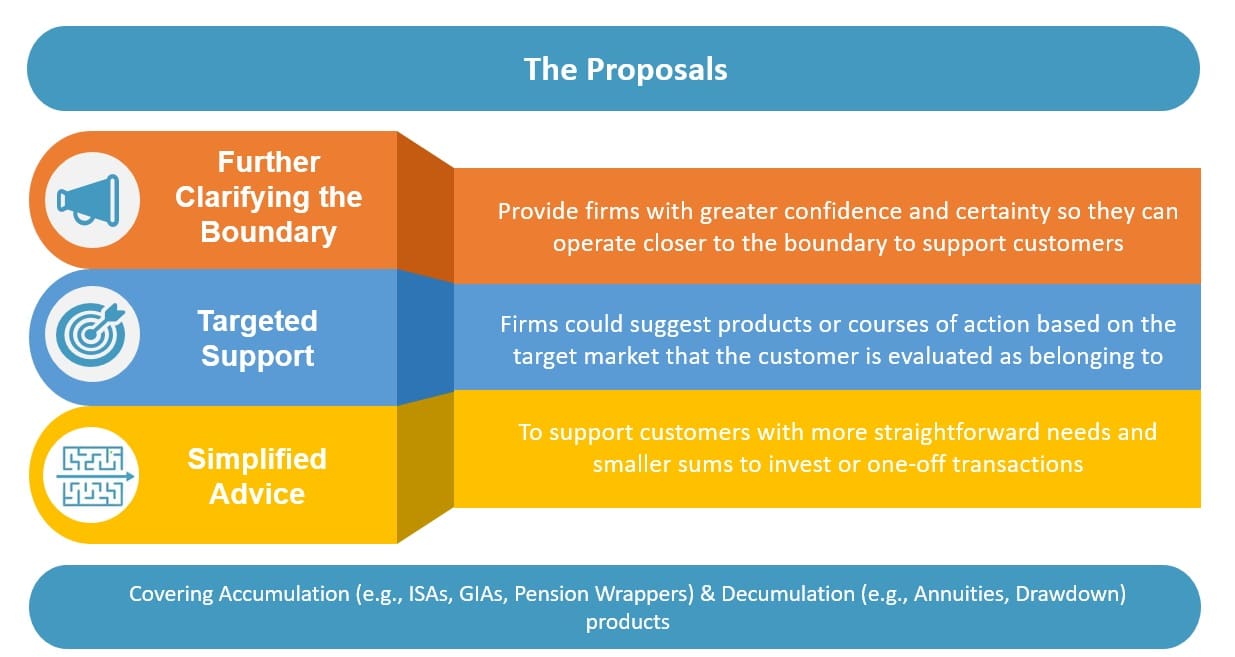

Last Autumn, the FCA published guidance and several working examples aimed at encouraging firms to get closer to the boundary in the support and guidance they provide to customers, whilst still complying with Consumer Duty principles. Subsequently, in December they released their Advice Guidance Boundary Review – proposals for closing the advice gap and ‘enabling consumers to access better support’, inviting interested parties to provide feedback by the end of February.

The Problem

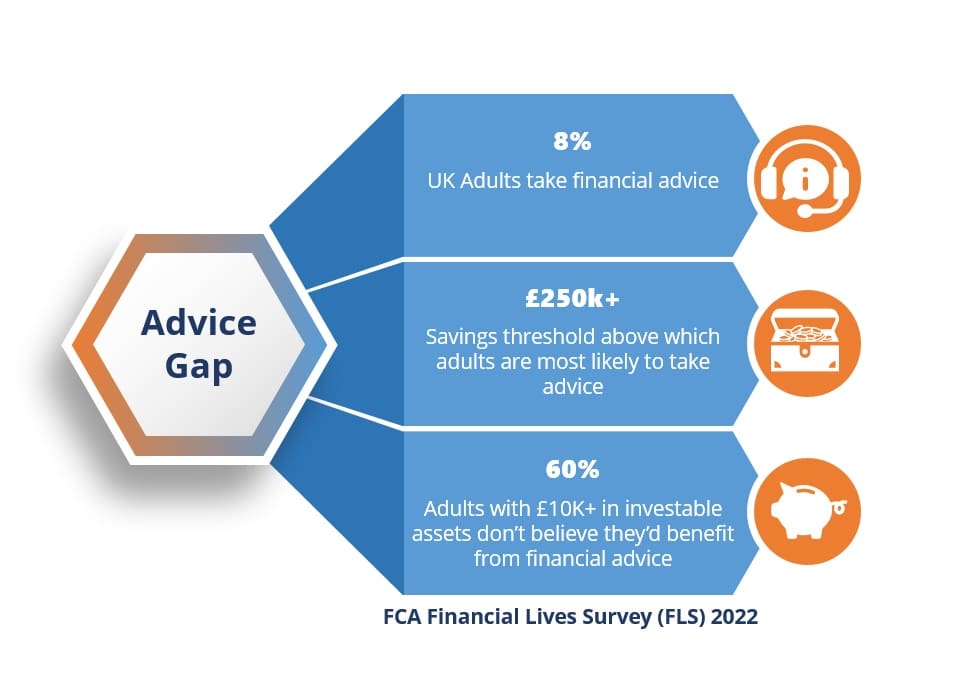

Ever since I started my career in financial services over 20 years ago, the advice guidance boundary has been problematic. Whilst the regulations are clearly there to serve a purpose, it undoubtedly makes firms hesitant in taking additional steps to support customers for fear of stepping too far into the murky grey area that is the advice guidance boundary

Industry Reaction

The proposals will pose challenges to both IFAs and investment platforms. The FCA have asked firms to suggest where more examples would be useful or if handbook rules would be preferable in some instances to provide legal certainty e.g. Fact Find requirements. Industry feedback has been clear that rules are preferred as opposed to guidance. With the current advice guidance boundary being subjective and open to interpretation, clarity is the key. If the outcome of the consultation provides clear definitions, expectations, rules, and worked examples; it will give firms more confidence to extend the help they provide to customers.

Targeted Support provides an opportunity for firms to make ‘people like you’ suggestions to customers having identified them as part of a given target market. Having spoken recently to Renny Biggins, Head of Retirement at TISA, TISA are very supportive of this proposal. According to the FCA, it has the potential to help all consumers who might have a need for help beyond that which can be provided by information or guidance. It will provide an opportunity for retail banks, life insurers and platforms to use customer data and product knowledge to provide greater support to consumers than is currently possible.

What might this look like in practice? Perhaps more ‘nudges’ could be included throughout customer journeys and as part of customer engagement to prompt customers to actively consider the possibilities available to them. Technology and innovation will play a key role to develop this proposal and make the process more efficient and beneficial to customer.

However, there’s a risk this could encourage firms to upsell their own products and deter people from searching whole of market options (bearing in mind cross-subsidisation practice was ruled out as part of RDR reforms). In such scenarios, I think it would be important that firms include caveats to state that comparable products are available from other companies and encourage the customer to do their own research.

IFA Perspective

There is nervousness around the proposed simplified advice regime. Some feel it would be difficult to provide a sustainable model and make it commercially viable.

Whilst 40% of firms have a formal pot size thresholds for new customers, there are firms out there that are trying to tackle the advice gap by making advice more accessible to those with smaller sums to invest.

Natasha O’Neill, IFA with Strategic Solutions, told us they already operate a ‘Starter’ category. This is defined as ‘Investors starting their financial journey with assets under £20,000’ to encourage people into getting help and for better outcomes with their money. They acknowledge this is a loss leader but are more aware of the advice gap. It provides access to an adviser (most of which are at least Chartered status) to help learn more about financial products and their options. Strategic Solutions are continually committed to helping the community and hope their ‘Starter’ category helps people have access when it is needed the most.

Clearly, providing advice without doing a full fact find and personal recommendation would increase the risk of inadvertently giving unsuitable advice, therefore financial advisers need legal certainty. The FCA have indicated that it would provide rules regarding the information firms would need from a consumer to provide simplified advice. This would help protect both the firm and the customer.

On a positive note, some in the industry believe that junior financial advisers could be utilised to support simplified advice, providing an opportunity for them to take on more responsibility and progress in their careers.

“This could be a good opportunity for new advisers and Paraplanners whilst helping decrease the advice gap, allowing more people to have access to help.”

Natasha O’Neill, Strategic Solutions

Simplified advice could also provide opportunities to deliver advice through other avenues. One use case for this could be employer supported sessions for employees at retirement, to help them understand their options.

“Some of our members want to offer simplified advice at retirement as it’s a big benefit to members.”

Renny Biggins, TISA

However, at this point pension decumulation options are excluded from the scope of simplified advice which seems like a huge, missed opportunity, and hopefully something that will change post-consultation.

Conclusion

Will these proposals have the desired effect of ‘enabling consumers to access better support’?

The proposals are a positive step in the right direction and should help close the advice gap by bridging the gap between non-tailored guidance that’s free to all and paid for, tailored advice that’s unaffordable for majority.

There’s political support from both parties on closing the advice and guidance gap, however this is only one piece in the puzzle. Other initiatives including financial inclusion and education, value for money, and customer engagement also need to be progressed alongside to help people grow in confidence, make better financial decisions, and achieve the best outcomes for their individual circumstances.

The FCA will likely publish the output from the consultation feedback in a few months’, and it will be interesting to see how they respond to industry suggestions and concerns. There will then be a sizeable amount of work to do to implement the proposals, particularly around simplified advice. As such, it’s likely that the proposals will be realised in tranches.

We believe that changes made as a result of this review could have a significant and positive impact, providing clarification for firms on what they can proactively do to support customers in making good investment decisions.

Talk to Simplify about how we can help you to best support your customers – get in touch at: [email protected].

References:

- Blackburn, Nicola; Sharif, Zachariah; Hagopian, Alicja. (2023). ‘It’s too risky for us’: IFAs on FCA’s advice-guidance reforms – citywire.com (Accessed 22/01/2024)

- (2023). Advice Guidance Boundary Review – FCA (Accessed 22/01/2024)

- (2023). DP23/5: Advice Guidance Boundary Review – proposals for closing the advice gap – FCA (Accessed 29/01/2024)

- (2023). Helping firms provide more support to customers making investment decisions –FCA (Accessed 22/01/2024)

- Gilbert, Jack. (2023). FCA to relax advice-guidance boundary in landmark review – citywire.com (Accessed 15/01/2024)

- Hawthorne, Stephanie. (2023). Redrawing the blurred boundary between guidance and advice – professionalpensions.com (Accessed 09/01/2024)

- Rach, Sonia. (2023). FCA helps firms navigate advice guidance boundary – FTAdviser (Accessed 29/01/2024)